From Concept to Completion: The Complete Financial Guide to Building Your Brisbane Home

Introduction

Building your dream home is one of life's most significant financial and emotional investments. Understanding not just when money flows throughout the project, but also how to structure your finances correctly from the outset, can transform what feels like an overwhelming process into a series of manageable, well-planned milestones.

In this guide, we're combining our expertise—the architectural team at Quorum Studios and Zoe Kowalski from MLN Finance—to walk you through the complete financial timeline of a residential build in Brisbane and South-east Queensland. From that first spark of inspiration to the day you turn your key in the lock, we'll show you what to expect, when to expect it, and how to finance it strategically.

Before You Begin: Getting Your Finance Structure Right

FINANCE PERSPECTIVE — MLN Finance

Best time to speak to a broker: 3 to 6 months before construction begins

Before we dive into the project timeline, let's address the foundation of your entire build: your finance structure. This is where many Brisbane clients make their first critical mistake—they commit to plans, engage an architect, and then discover the bank won't fund the project the way they expected.

Understanding Your Loan Structure Options

There are several ways to finance renovations and custom builds in Brisbane. The best option depends on your project scale, existing equity position, and whether you're building on land you own or purchasing new land.

Construction or Renovation Loan (Progress Payments)

Best for major renovations, extensions, and structural changes. Funds are released in stages as construction progresses, and you usually only pay interest on the amount drawn down. This is the most common structure for new builds and substantial renovations.

Refinance to Renovate (Equity Release)

One of the most common options in Brisbane. If you have sufficient equity in your existing home, refinancing can unlock funds for renovations and may also reduce your interest rate or improve cash flow. This works particularly well when you're staying in your home during renovation.

Home Loan Top-Up

A simpler option when staying with your current lender, often suited to smaller renovation budgets. Processing is typically faster, but you're limited to what your current lender will approve.

Line of Credit (LOC)

Useful for flexible or staged renovations where you want to draw funds as needed. Not all lenders offer these anymore, and policies vary significantly, so professional guidance helps navigate options.

Bridging Finance

Can work well for knockdown rebuilds or major renovations where you need funds before selling your current property. Policies differ significantly between lenders, and this is typically more expensive but provides crucial flexibility.

The Importance of Choosing the Right Lender

Here's something many clients don't realise: lender construction policies vary dramatically. Choosing a lender based purely on interest rate can be a costly mistake when it comes to construction finance.

Some lenders have strict documentation requirements. Others push back on unusual inclusions or high-end finishes. I once had clients wanting to finance a ceiling-to-floor fish tank, including the fish, through their construction loan. Needless to say, fish are very hard to convince a bank to use as security.

It's a funny example, but it highlights an important point: lenders are specific about what they will and won't fund. The right finance strategy considers lender construction policies, valuation approaches, and progress payment structures—not just the advertised rate.

Pre-Approval vs Pre-Qualification

Before committing to design fees, get finance pre-approval (not just pre-qualification). Pre-qualification is a soft assessment based on what you tell the bank. Pre-approval involves documentation review and confirms exactly what you can borrow. This clarity is essential before investing tens of thousands in design fees.

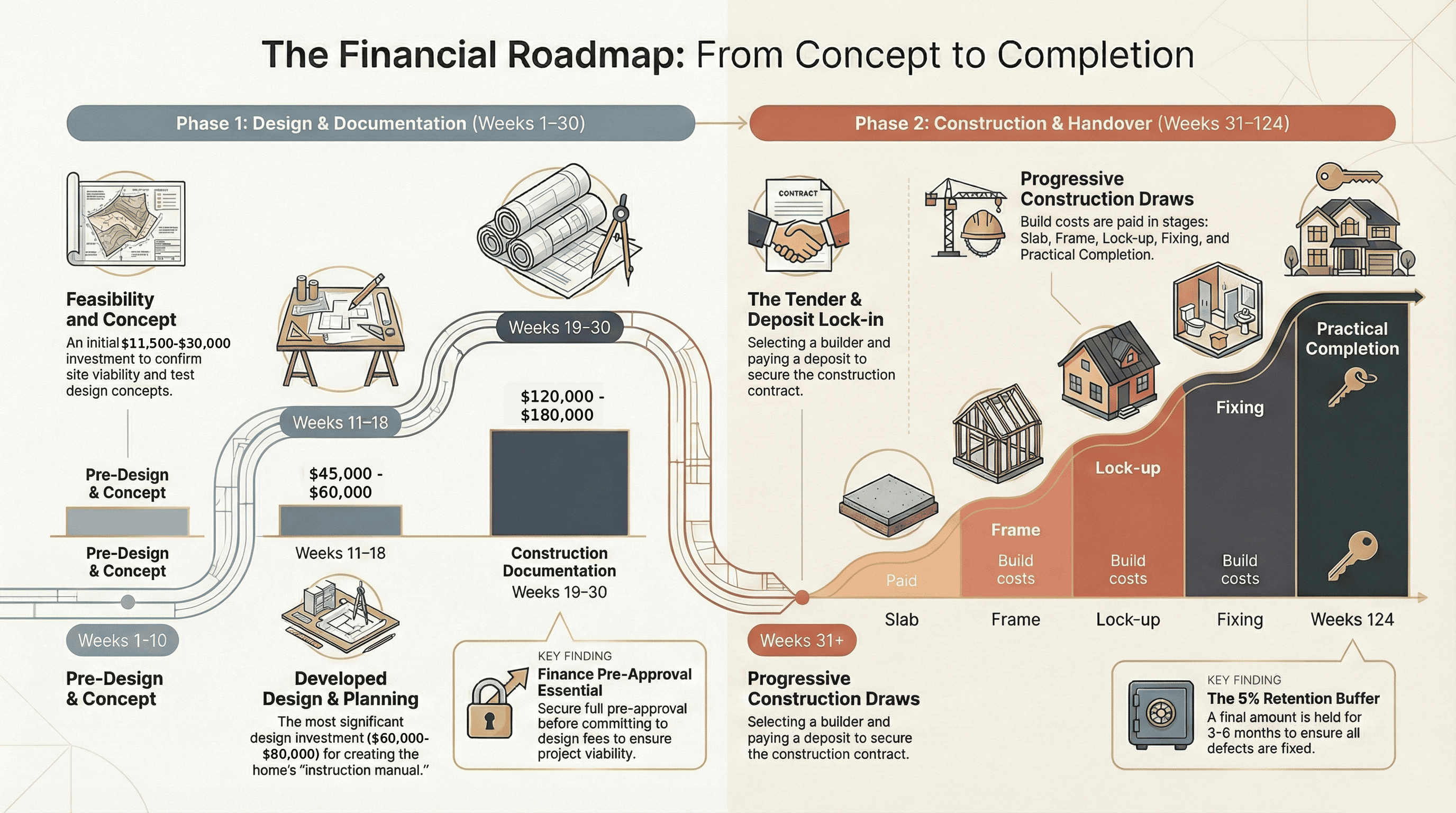

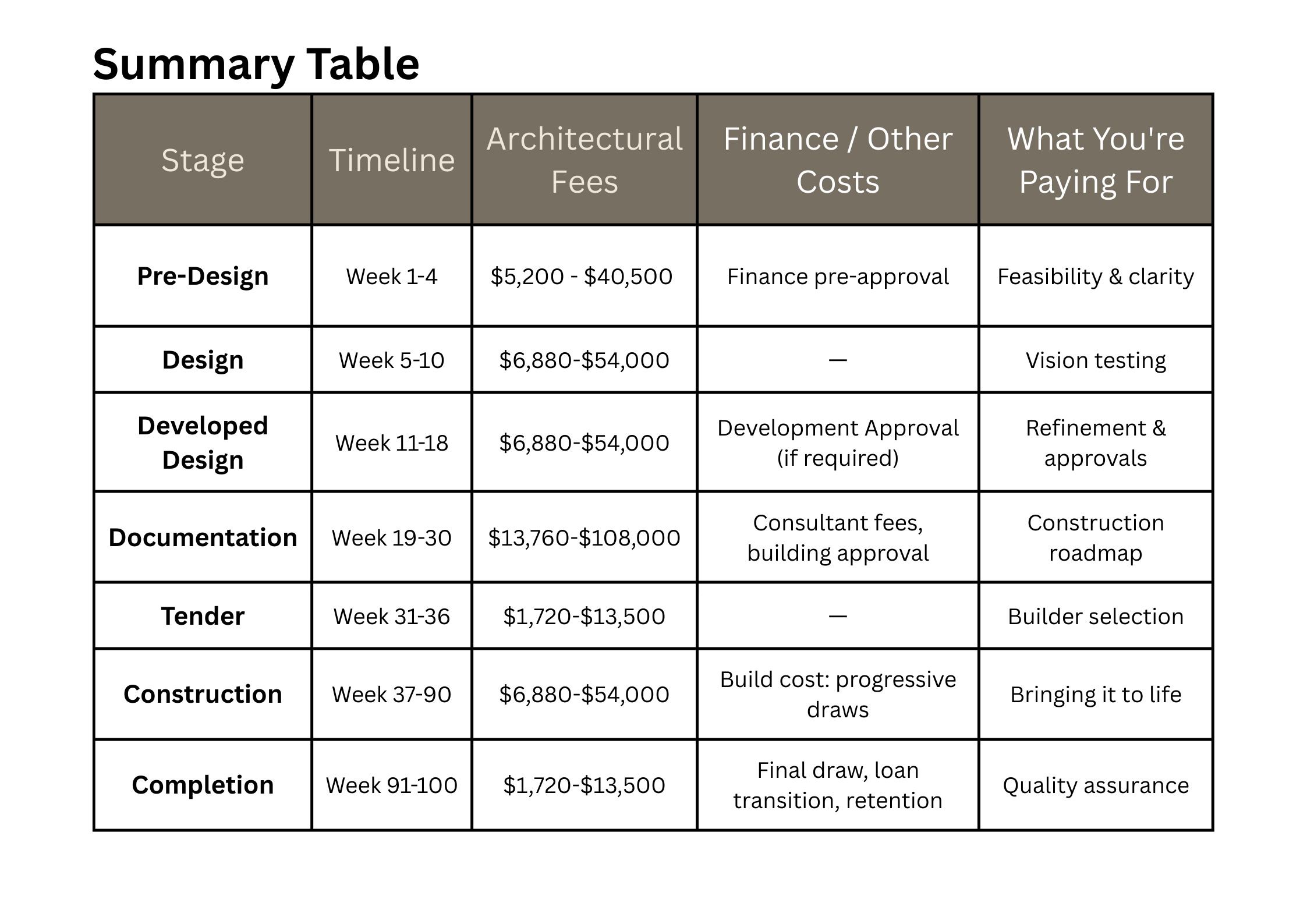

Stage 1 - The Pre-Design Phase: Laying Your Foundations (Week 1-4)

ARCHITECTURAL PERSPECTIVE — Quorum Studios

Before we sharpen a single pencil or open a CAD file, we're asking the most important question: How do you want to live?

This isn't about floor plans yet—it's about understanding your lifestyle, your family's rhythms, how you entertain, where you work and play, and how you move through your space. We're also conducting feasibility studies: What does your site allow? What are the planning constraints? Is your vision achievable within your budget?

What you're investing in:

- Initial consultation and site analysis

- Feasibility assessment

- Preliminary budget discussions

- Understanding council requirements for your area

Typical investment: 10-15% of total architectural fees, usually about $5,200 - $40,500 (depending on project complexity; for instance, a renovation of a protected Queensland Heritage home often commands a higher fee due to stringent council requirements).

Why this matters financially: Before we start designing, you need to know if you actually have a project. Can your site accommodate what you're imagining? Does the council overlay allow it? Are there drainage issues or easements that kill the concept before it starts? Is your budget realistic for your vision?

This groundwork determines whether you proceed or not. We've seen clients ready to commit $100K+ in design fees only to discover their site can only fit a house half the size they need, or that heritage constraints make their vision impossible. Getting these fundamentals sorted first means you're only investing in design when you know you have a viable project worth designing.

FINANCE PERSPECTIVE — MLN Finance

This is the ideal time to confirm your borrowing capacity and equity position. At this stage, we verify which lenders suit your specific project type and help you understand any limitations before you commit to detailed design.

For example, if your project includes unique features—a large basement carpark, commercial-grade workshop, or high-end finishes—some lenders will have different appetites and valuation approaches. Knowing this early prevents disappointment later.

Financial Milestone:

- First payment to architect: $5,200 - $40,500

- Secure finance pre-approval (not just pre-qualification)

- Confirm borrowing capacity before proceeding to design

You're spending a few thousand now to avoid potentially wasting tens of thousands on a project that was never viable in the first place. At the end of this phase, you'll make the decision: do we have a project worth proceeding with, or do we need to rethink our approach?

Stage 2a - Design: Bringing Vision to Life (Week 5-10)

ARCHITECTURAL PERSPECTIVE — Quorum Studios

This is where your vision starts taking physical form. We're creating initial sketches, exploring spatial relationships, and testing different approaches to your site. You'll see preliminary floor plans and maybe some 3D visualisations to help you understand how spaces will feel.

At Quorum Studios, we work collaboratively—often bringing in a builder early to get preliminary cost estimates and structural engineers to ensure what we're imagining is achievable. This isn't just an architectural exercise; it's a feasibility-tested concept.

What you're investing in:

- Concept design drawings

- Preliminary cost estimates (in collaboration with builders)

- Multiple design iterations based on your feedback

- Early consultant coordination (engineer, surveyor as needed)

Typical investment: 15-20% of total architectural fees, usually $6,880-$54,000.

Why this matters financially: Before we go further, you need to know if this concept works within your budget. If preliminary estimates come back too high, we can adjust now rather than after you've invested in detailed documentation. We've seen clients fall in love with designs that would cost $4.5M to build when their budget is $2M. Starting with clarity prevents heartbreak—and wasted fees—down the track.

FINANCE PERSPECTIVE — MLN Finance

During this phase, we're ensuring the concept aligns with lender valuation expectations. It's important to understand that a renovation or build costing $200k does not automatically add $200k in value. This is where an architect and broker working together can help avoid overcapitalising.

Brisbane suburbs have valuation ceilings—the maximum price properties typically achieve regardless of how much you spend. Building a $5M home in a suburb where comparable sales top out at $3.5M creates a valuation gap that lenders won't fund. We help you understand these limitations while your design is still flexible.

Financial Milestone:

- First substantial design fee instalment: 15-20% of architectural fee

- Review preliminary build costs against borrowing capacity

- Adjust the scope if needed before committing to detailed documentationStages 2b and 2c – Developed Design: Refining the Details (Week 11-18)

ARCHITECTURAL PERSPECTIVE — Quorum Studios

Now we're getting serious. Floor plans are refined, elevations are detailed, and materials are selected. You're making decisions about kitchen layouts, bathroom fixtures, window placements, and ceiling heights. We're coordinating with structural engineers, hydraulic consultants, electrical designers—everyone who needs to have input before we document.

This is also when we're preparing for town planning if your project requires council approval.

What you're investing in:

- Detailed design development drawings

- Material and finish selections

- Consultant coordination (structural, hydraulic, electrical)

- Town planning application preparation (if required)

Typical investment: 15-20% of total architectural fees, usually $6,880-$54,000.

Why this matters financially: This is your last chance to change your mind affordably. Once we move into construction documentation, every change becomes expensive—we're redrawing coordinated consultant drawings, resubmitting to council, and potentially re-pricing with builders.

A bathroom layout change in this phase? A few hours of revision. The same change after documentation? It could cost you $60,000-$120,000 in re-documentation fees alone.

We've had clients engage us after their previous architect or designer rushed this phase, lodged incomplete applications, and then had to redesign based on council feedback—adding months to the timeline and doubling their design fees. This phase is about making all your decisions while they're still relatively easy to change.

FINANCE PERSPECTIVE — MLN Finance

At this stage, we're preparing your lender-ready documentation package. Construction and renovation loans are documentation-heavy, and missing one item can delay approvals significantly.

Common lender requirements include:

- Architectural drawings

- Builder quote and contract (preliminary at this stage)

- Scope of works and specifications

- Itemised cost breakdown

- Council approvals were required

- Detailed specifications for materials and finishes

Better documentation often supports a better valuation outcome. When plans clearly show quality finishes, thoughtful design, and appropriate scale for the suburb, valuers can more confidently assess the "as completed" value.

If your project includes sustainability features—such as solar panels, batteries, high-performance insulation, or energy-efficient design—this is the time to discuss green loan options. Many lenders currently offer competitive rates for energy-efficient builds, and some provide additional borrowing capacity for sustainability upgrades.

Financial Milestone:

- Second major fee instalment: 15-20% of architectural fees

- Development application fees, if applicable

- Preliminary lender documentation submitted

- Consultant fees for structural, hydraulic, and electrical design

Stage 3 - Documentation: Building the Blueprint (Week 19-30)

ARCHITECTURAL PERSPECTIVE — Quorum Studios

This is where we create the complete instruction manual for your home. Every wall, every window, every connection is documented. We're producing construction drawings, specifications, schedules—everything a builder needs to accurately price and construct your project.

We're also coordinating building certification and obtaining your building approval.

What you're investing in:

- Complete Issue for Construction (IFC) drawing set

- Specifications document (detailing materials, finishes, fixtures)

- Coordination with the certifier for building approval

- Tender/pricing package for builders

Typical investment: 35-45% of total architectural fees, in the range of around $13,760-$108,000.

Why this matters financially: This is the last checkpoint before financial commitment. Once builders quote from these documents, you'll know your real build cost and can finalise your construction loan.

FINANCE PERSPECTIVE — MLN Finance

Once documentation is complete, the bank usually orders an "as completed" valuation based on the proposed plans. This is different from a standard property valuation—the valuer considers:

- The quality of the proposed renovation or build

- Comparable sales in your suburb

- The ceiling price in your area (what properties actually sell for)

- Whether the scope matches the neighbourhood character

- Professional quality of documentation

This valuation determines your actual borrowing capacity for construction. It's why we emphasise getting finance advice early—we can identify potential valuation issues before you've invested $160,000 in documentation.

At this stage, we're also finalising your loan structure. If you're doing a construction loan with progress payments, we'll align the draw schedule with your builder's payment milestones. If you're refinancing to renovate, we're ensuring the equity release timing matches your payment obligations.

Financial Milestone:

- Third major fee instalment: 35-45% of architectural fees

- Building certification fees

- Bank orders "as completed" valuation

- Construction loan formally approved

- Final borrowing capacity confirmed

Stage 4 – Tendering & Contract: Locking It In (Week 31-36)

ARCHITECTURAL PERSPECTIVE — Quorum Studios

We're helping you navigate builder quotes, compare apples with apples, and make sure you understand exactly what you're getting. This isn't just about price—it's about value, quality, and who you'll be working with for the next 12-18 months.

Once you've selected your builder, you'll need to review the building contract to ensure it aligns with the documented design.

What you're investing in:

- Tender analysis and builder selection advice

- Contract review and coordination

- Pre-construction meetings

Typical investment: Often included in the overall fee structure, or 5-10% of construction cost.

Why this matters: An architect's involvement during the tender process helps mitigate the risk of builders not pricing the same scope of work, allowing for genuine comparison, and ensures that technical details are properly understood before construction begins. This oversight protects the client from incomplete quotes, scope gaps, and costly variations that arise when builders make different assumptions about what's included.

FINANCE PERSPECTIVE — MLN Finance

Once you've accepted a builder's quote, your construction loan moves to final approval. The bank reviews the building contract to ensure it matches the valuation scope and that progress payment milestones are appropriate.

Key aspects we verify:

- The builder's quote matches the documentation scope

- The progress payment schedule aligns with lender requirements

- The contract includes appropriate insurance coverage

- Retention clauses protect your interests

- The variation process is clearly defined

Some lenders have strict rules about builder credentials, insurance requirements, and contract terms. Choosing a lender who understands high-end residential construction means smoother approvals and fewer surprises.

Financial Milestone:

- Builder's deposit: typically 5-10% of construction cost

- Construction loan formally executed

- First progress payment schedule confirmed

- Allow contingency funds for variations (typically 10-15% of build cost)

Stage 5 - Construction: Watching It Rise (Week 37-90)

ARCHITECTURAL PERSPECTIVE — Quorum Studios

Should you choose to engage your architect for contract administration, we're your eyes on site, conducting regular site visits, answering builder questions, assessing variations, and ensuring what's being built matches what we designed.

This is also when those inevitable site decisions happen—that wall colour looks different in real light, or you've decided you want that window just a bit larger.

What you're investing in:

- Contract administration

- Site inspections (frequency depends on your contract)

- Response to builder queries

- Assessment of variations

- Practical completion certification

Typical investment: 20-35% of total architectural fees, usually in the $6,880-$54,000 range, paid in stages through construction

Why this matters: The architect ensures what's being built matches the approved drawings and maintains the design vision when site conditions require changes. Builders often need to make small decisions or substitutions—without the architect present, these can compromise the design or quality.

FINANCE PERSPECTIVE — MLN Finance

Construction loans release funds in stages as the building progresses. Typical progress payment milestones include:

- Slab/Base Stage – After the concrete slab is poured (or stumps/footings for elevated homes)

- Frame Stage – Once the timber or steel frame is complete

- Lock-up Stage – When the building is weatherproof (roof, windows, doors installed)

- Fixing Stage - Internal fit-out substantially complete (kitchen, bathrooms, flooring)

- Practical Completion – Building complete and ready for occupation

- Final Completion - After defects liability period (3-6 months)

At each stage, the builder requests payment, the bank sends an inspector to verify work completion, and funds are released. This protects you from paying for work not yet completed.

During construction, you're typically paying:

- Interest only on drawn amounts (not the full loan)

- Architectural contract administration fees

- Any approved variation costs

- Your existing home loan (if renovating your current property)

This is where lender construction policies really matter. Some banks require extensive documentation at each draw. Others have streamlined processes. Some release funds quickly; others take weeks. Choosing the right lender early makes this phase far less stressful.

Financial Milestone:

- Progressive payments at each construction stage

- Interest-only payments on drawn construction funds

- Variation costs as approved

- Regular budget review to avoid cost overruns

Post-Construction / Completion (Week 91-100)

ARCHITECTURAL PERSPECTIVE — Quorum Studios

At this stage, final inspections are being conducted, creating a defects list, and ensuring everything is finished to standard. Once satisfied, you'll be issued your Practical Completion certificate. After a defects liability period (usually 3-6 months), one final inspection is done, and you'll be issued the Final Completion certificate.

What you're investing in:

- Final inspections

- Defects assessment

- Practical and Final Completion certification

Typical investment: Final architectural fee instalment, usually 5-10% of total fees, usually in a range of $1,720-$13,500. This covers both the Practical Completion and the Final Completion inspection that happens after the defects period.

FINANCE PERSPECTIVE — MLN Finance

At Practical Completion:

- The final progress draw is released to the builder (typically 10-15% of the construction cost, often $500,000-$750,000 on a $5M build)

- Retention amount held (usually 5%, held for 3-6 months during defects liability period)

- Your construction loan now converts to a standard home loan

- Principal and interest payments begin (your interest-only construction period ends)

- The bank conducts a final valuation to confirm the "as built" value

After Defects Liability Period (Final Completion):

- Retention released to the builder

- Final architectural certification provided to the bank

- Opportunity to refinance if better rates are available

- The construction loan formally closed

This is also when many clients review their overall financial position. You've just completed a major investment, and your property value has (ideally) increased significantly. This may create opportunities to:

- Consolidate other debts at better rates

- Access additional equity for other investments

- Refinance to a more competitive home loan product

- Review your overall financial structure with the increased asset value

The Complete Financial Picture: What to Budget

Total Architectural Investment: $43,040-$337,500 (typically 6-15% of construction cost for full service)*

*Architectural fees do not include consultant fees, council fees, or construction costs

Additional Finance Costs to Budget:

- Lender application fees: $600-$1,200

- Valuation fees: $800-$2,000 (depends on property type)

- Construction loan establishment: Typically $600-$1,000

- Progress inspection fees: Often $150-$300 per draw (5-6 draws typical)

- Legal fees for contract review: $1,500-$3,000

- Contingency for variations: 10-15% of construction cost ($500,000-$750,000)

Your Construction Finance Checklist

If you're planning a custom renovation, extension, or new build in Brisbane:

✅ Speak to a Brisbane mortgage broker early (3-6 months before construction begins)

✅ Confirm borrowing capacity and equity position before committing to design fees

✅ Choose the right lender based on construction policy, not just interest rate

✅ Select the right loan type (construction loan vs refinance to renovate vs other options)

✅ Prepare detailed plans, specifications, and costings to support valuation

✅ Understand valuation expectations and suburb price ceilings to avoid overcapitalizing

✅ Align loan structure with construction timeline and progress payment schedule

✅ Allow contingency funds for variations and unexpected costs (10-15% of build cost)

✅ Discuss green loan options if the project includes solar, batteries, or energy-efficient design

✅ Review builder contract terms to ensure they align with lender requirements

✅ Plan for loan conversion from interest-only construction to principal & interest at completion

Final Thoughts

From the Architects — Quorum Studios

The financial journey of building isn't just about having enough money—it's about having the right money at the right time. Every phase builds on the last, and understanding this timeline helps you plan not just financially, but emotionally and logistically too.

Our collaborative approach means we're having budget conversations from day one, bringing builders in early, and making sure your vision aligns with your reality before you're too far down the track.

At Quorum Studios, we believe the question "How do you want to live?" extends beyond design to encompass your complete investment. We want you to love your home and feel confident about the financial decisions that made it possible.

From the Broker — MLN Finance

A considered renovation or custom build deserves a finance strategy that supports the design from the very beginning. Because lender construction guidelines vary so widely, the right advice early can help you avoid delays, maximise borrowing power, and ensure your finance supports the build from start to finish.

Working alongside boutique architectural studios like Quorum Studios, I help clients align lender requirements, valuations, and loan structure, ensuring the funding process complements the build rather than delaying it.

Many lenders currently offer competitive construction and renovation loan pricing, and some provide sustainability-focused products that support energy-efficient upgrades. The right structure—matched to your specific project—makes all the difference.

Ready to Start Your Journey?

Whether you're just beginning to think about building or you're ready to take the first step, understanding this timeline gives you the confidence to move forward.

Quorum Studios — [07 3062 9431, admin@qstudio.au]

Architecture for the way you want to live

MLN Finance - Zoe Kowalski — [0498 694 548, zoe@kowalskifinance.com]

Construction finance expertise for Brisbane builds

Disclaimer: This guide pertains to typical residential projects in Brisbane and Southeast Queensland. It is important to understand that each project is unique, and timelines and costs may vary based on site conditions, design complexity, and council requirements. The dollar value figures in this guide are based on a range reflecting entry-level project homes, up to an average of $1.8 million for newly built homes. All information is accurate as of 2025.